Nov. 11, 2014 original publish date.

June 6, 2015 typo corrections

10 Things Congress Can Do to Reduce Health Care Costs Now

original article written by Net Advisor™

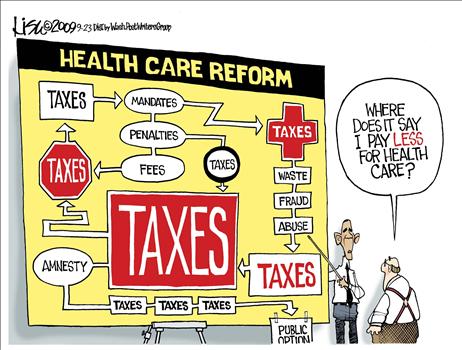

WASHINGTON DC. There is much talk about healthcare, specifically “Obamacare” and the push to repeal and replace it. The costs of government healthcare spending exceeded $10.6 Trillion in President Obama’s first four years. Clearly even with the passage of ACA “Obamacare,” costs and spending are going up at a rate of $100 Billion more per year from 2009-2012.

Most of healthcare costs are due to the uninsured, yet everyone else is currently being forced to pay this. The Obamacare healthcare law was based on a deception from day one.

The architect of Obamacare, John Gruber said on camera that the intent of the (Obama) healthcare law was to deceive the American public in order to get it passed, and consumers are still being misled about the true costs of their government ran healthcare.

President Obama erroneously said that healthcare premiums could fall as much as 3,000% (Video). That statement is untrue. In insurance math you can’t have a negative premium. A premium could theoretically only fall up to 100% then it is free. Any number below zero would mean the insurance company is paying you to have the policy.

Seniors are also being affected by government-ran healthcare in terms of higher costs. In 2015, Obamacare will cut $1.35 Billion from California seniors enrolled in Medicare Advantage says California Congressman Darrell Issa.

Jobs are also being hurt by a healthcare law that was not supposed to kill American jobs, and the total impact on the U.S. economy and the national debt is damaging.

President Obama has admitted that the government is not as efficient as the private sector. Thus we should move healthcare back to the private sector and Congress can write healthcare laws that are more friendly to the consumer, the pharmaceutical companies and insurance companies where we can all save money.

Here Are 10 Things Congress (and the President) Can Do to Reduce Heath Care Costs Now

1. Force Market Competition. Allow consumers to be able to buy health insurance across state lines = Drives competition. Currently many states may have one to three or so insurance companies to choose from. That isn’t competition, that is an oligopoly. By allowing consumers to buy insurance from other states forces competitive pricing.

My only big concern here is that insurance companies will then start a wave of mass mergers to reduce competition. But a competitive environment is better for consumers than a non-competitive environment.

2. Extended Premium Contracts. Consumers should be able to “lock in” contract rates for more than one year. Insurance companies have extensive underwriters and actuaries that provide statistical analysis to manage insurance risks including cost projections. These departments should be able to make longer-term contracts with fixed premiums with a known fixed cost for consumers. Rates may be based on age and overall health.

Consumers could then lock in rates for two, three, up to maybe five years or whatever the insurance company (or government) allows. This helps consumers with longer term financial planning when it comes to health insurance costs.

3. On-Line Shopping Cart Riders. A Rider is a feature that can be added to an insurance policy. Some people may not want certain riders such as covering a sex change, or male maternity coverage in case he gets pregnant. Women may not want to pay for prostate exams. This universal care covering everything for everyone costs money – and a lot of money.

Creating on-line shopping carts where consumers can pick and choose a base plan to premium plans and then add or remove riders at stated costs for their age and health allows the consumers to pay for what they want. This can keep costs down for the consumer and insurances company don’t have to pay for coverage people don’t want. A rider can be added or deleted on each contract renewal date and covers for the contract period.

4. Pre-Existing Conditions. Insurance companies cannot cancel your healthcare plan because of a condition that occurred after insurance became effective, so long as the patient did not intentionally deceive or defraud the insurance company. Those with pre-existing conditions should not be turned down insurance, however they should pay more because they are using more services. For financial hardship for lawful citizens, states can look at subsidies if they so choose.

5. No Corporate Welfare. Insurance companies will not be guaranteed any profit from the government. Profits or losses are based on the success or failure of the insurance company.

6. Employer Deduction. This may or may not already exist under current law, but if not: All employer contributions are 100% tax deductible dollar-for-dollar. What this means is if an employer has one or more employees, has a company sponsored healthcare plan, and that employer is paying for healthcare on a pre-tax basis to employees, that healthcare paid for by the employer should be 100% tax deductible for the employer.

What this does is two things: (1) Creates an incentive for employers to receive a full pre-tax deduction if willing to pay part or all of the monthly insurance premiums for employees in a sponsored plan. (2) It creates an incentive for employees to want to stay with a company who is covering their monthly healthcare premiums.

7. Fitness Incentive. Gym memberships, college classes involving sports, athletics and the similar should be fully tax deductible. Diet and lifestyle have a huge impact on health. Thus provide an incentive for the public that encourages them to be more active. A more active person may have the tendency to, or at times be conscious of diet in order to improve their performance. Even some moderate exercise can contribute to better health. Thus, attention to better health can reduce the need for certain doctor’s visits, which intern helps reduce healthcare costs.

8. Reform Health Savings Accounts (HSA). This is a big one and probably among the most important ways to reduce healthcare costs long-term. Here is a general outline:

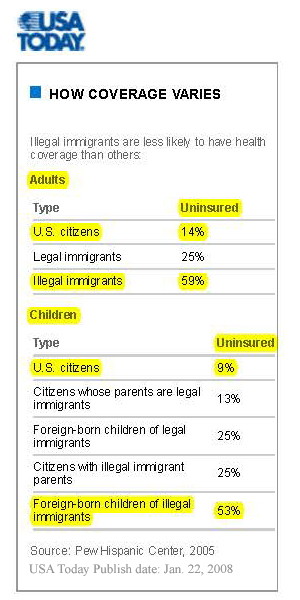

- Everyone living in the United States or U.S. territories qualifies for HSA. Yes, I am giving this to illegal aliens living in the USA too because they are a big part why healthcare costs are high. The U.S. is not going to mass deport millions of illegal aliens living in the USA, even though that is what federal law requires the government to do. This is not granting citizenship or amnesty, just to comply with at least one law and help everyone with healthcare costs. A tax ID number will be required to open an account since a HSA involves potential taxes and the IRS. Tax ID’s are free and the IRS is more than happy to give you one.

- HSA’s may be set up by employers, banks, insurance companies, securities brokers and registered third party administers (more jobs created?).

- Set up either a pre-tax or after tax account or both subject to split contribution limitations. Pre-tax money comes out of a paycheck, is not subject to tax but could be later on as I explain shortly. After tax money should not be taxed since it was already taxed once. Gains in a HSA could be taxed under certain conditions.

- HSA Contributions. Up to 10% pre-tax or up to 20% after tax income may be deposited into an HSA. This contribution number needs to be high for people to actually save for the outrageous healthcare costs they are likely to face one day, like now. Contribution rates can be reset by the consumer once annually. Perhaps a minimum contribution of 2% should be considered. We’re going to pay for healthcare costs one way or the other; and we might as well have at least a bare minimum that helps defray the cost of our own healthcare with our own money.

- Matching Contribution. Employer-based plans could have an optional matching contribution that is fully tax deductible for the employer contributing the matching funds. Some employers contribute matching contributions to retirement plans, why not have one for healthcare plans too? This creates incentives for employees to contribute to their healthcare plan, thus sets aside money for employee’s healthcare costs. A vesting schedule may be used to create incentives for employee loyalty in exchange for company matching contributions.

- Distributions are tax free for qualified medical expenses. HSA withdrawals should be allowed to cover health insurance premium payments, co-payments, long-term care, and the similar.

- There unfortunately has to be disincentives for those who use HSA accounts for other than it was intended.

- Limited withdrawals for non-health emergencies (non-qualified withdrawal) subject to IRA-style penalties. One has to create a disincentive to withdraw money that is supposed to be saved for healthcare costs, not for living in the moment (buying a car, rent, or a new iphone). If need an account to save for future general living obligations or entertainment, open a savings account, not a health savings account.

- Non-qualified distributions subject to 20% tax penalty and additional 10% if under 55.

- Non-qualified distributions on inherited accounts subject to 30% tax penalty and additional 10% if under 55.

- Money may be invested ‘conservatively’ based on age (new money manager and industry-related jobs?).

- Maximum account size limit HSA, maybe $5 million adjusted annually for inflation (CPI). Excess account size limits on gains subject to ordinal income or long-term capital gains tax. Purpose: Fund for disaster although most not likely to hit this amount. Having a large cap limit allows covering current and in some cases future healthcare costs for future related generations as I will discuss more here.

- You can have any insurance health policy or no insurance policy to have a HSA under my plan.

- Unlike current policy, you can have an HSA if you have Medicare or state government care.

- All accounts are separate account and forever owned by the account holder. Thus if divorced, the account is still maintained by the person who has the account in their name. If married, must equally contribute to both spousal accounts if only one spouse is working (Work out income details).

- Minimum annual deductible on healthcare policy: $0.00. It should not matter what your healthcare deductible is, the HSA should be permitted to cover your healthcare costs which includes monthly premiums.

- Policy shall not discriminate in any way whether single, married, family or no family.

- Policy may apply to health, disability (short or long-term), dental, vision or long-term care costs.

- All prescription drugs covered. Marijuana is not covered as currently deemed illegal under federal law, and HSA’s are regulated by the IRS, thus subject to federal law.

- High-income tax shelters limitations. If annual income has averaged (say) $1 million or more in a year, maximum $25,000 / year contribution (again, these is just an example). A person who makes this income now, may not have this income 10, 20, 30 years from now, they too should have access to an HSA, and should not be discriminated against because of their income.

- Death of HSA owner. Account transfers tax free to legal spouse or current registered domestic partner.

- Death of HSA owner with child(ren). Account transfers tax free to HSA’s legal (adopted or biological) children (equally).

- The last two items above is a way to pay for healthcare costs without bankrupting future generations. This helps keep one’s long-term healthcare costs manageable, because people will have money in this HSA to pay for such costs. No need for these people to rely on government welfare programs when money saved from generations can be passed to pay for future generalizations’ healthcare needs. ConsumerAffiars.com cited a Harvard University study that suggested 62% of consumer bankruptcies are caused by healthcare-related expense problems. This generational transfer of HSA’s can help solve this problem.

- If one has no current spouse, registered domestic partner or legal children, any other pre-named or unnamed beneficiary subject to estate tax at current rate for full market value upon death of account owner OR continue using the HSA as outlined hereto.

9. More Free Market Competition. (1) Allow consumers to purchase prescriptions drugs from Canada’s government licensed pharmaceutical companies. This is already being done in some areas, but some states or plans may have restrictions. Many prescription drugs are lower cost in Canada than in the USA. Why should consumer be prevented from buying the same prescribed drug for substantially more money in the USA when it is available for less from our neighbor up north?

(2) Allow U.S. pharmaceutical companies direct sales to consumers with a medical prescription. Retail drugs will have all kinds of mark-ups from various distributors and other middle-persons. These costs of pharmaceuticals can be reduced with direct sales from the manufacture or their dedicated subsidiary (more job creation) to consumers who have a valid prescription.

10. Remove all taxes and penalties from existing healthcare law. There is apparently bi-partisan support to remove the medical device tax that affects the elderly, especially those on fixed income the most. Consumers should not have to pay a tax on top of their healthcare premiums, or on co-pays or other healthcare. We don’t need to add new taxes to the already costly healthcare. True disclosure and transparency of healthcare costs should be clear to consumers.

If Congress would like more suggestions or assistance, I’m available.

About the Author:

NetAdvisor™ previously held 3 insurance licenses and 6 securities licenses including two in securities compliance and management oversight. See bio.

Share this report on Facebook and Twitter. Thank you!

Reports:

- Is ObamaCare Killing Jobs?

- ObamaCare is an Example of Groupthink Gone Wrong

- Healthcare Education Series – What you need to know. Multi-part edu series.

Images/ graphics copyright by their respective owner.

Original article content, Copyright © 2014-2015 NetAdvisor.org® All Rights Reserved.

NetAdvisor.org® is a non-profit organization providing public education and analysis primarily on the U.S. financial markets, personal finance and analysis with a transparent look into U.S. public policy. We also perform and report on financial investigations to help protect the public interest. Read More.

{kind=link}